The Tax Court of Canada in October last year released its reasons for judgment in Brent Kern Family Trust v. Canada [2013] T.C.J. No. 286. The case was the TCC’s first opportunity to review and apply ...

The Tax Court of Canada in October last year released its reasons for judgment in Brent Kern Family Trust v. Canada [2013] T.C.J. No. 286. The case was the TCC’s first opportunity to review and apply ...

Advocate Daily initially originally published, "Tax court should go further when awarding costs”, in March 2014. Although a recent Tax Court of Canada decision shows a continued trend towards higher c...

The Income Tax Act (“ITA”) provides various tax advantages to corporations that qualify as Canadian-Controlled Private Corporations (“CCPC”).

Late last year, the Tax Court of Canada released its reasons for judgment in Ironside v. Canada [2013] T.C.J. No. 298, and Gouveia v. Canada [2013] T.C.J. No. 353. In Ironside and Gouveia, the Tax Cou...

The Canada Revenue Agency (“CRA”) announced, and now initiated, its 5th Annual Letter Campaign (the “Campaign”).** The CRA is in the process of sending 33,000 letters to taxpayers that have claimed bu...

Advocate Daily originally published “New CRA tools may mean more tax haven proceedings” in December 2013. Although the Canada Revenue Agency has reportedly struggled to deal with the number of cases i...

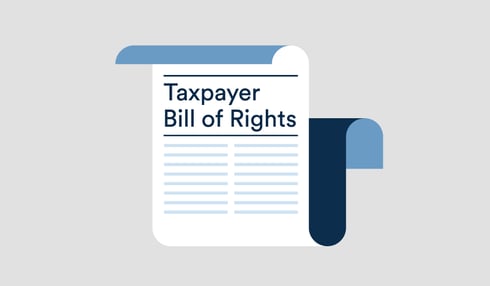

Eighteen new words have been added to the Taxpayer Bill of Rights, and Canada’s Taxpayers’ Ombudsman Paul Dube is hoping they will convince hundreds and perhaps even thousands more individuals and bus...

In cases heard under the TCC’s general procedure (as opposed to the informal procedure), the winning party may receive more than the amount of taxes in dispute plus interest—that is, the court may awa...

In its first decision on third party penalties, the Tax Court of Canada has curtailed the power of the Canada Revenue Agency; as expected, the CRA has already decided to appeal.

We have experience representing SR&ED claimants at the objection and appeal stages. At times, we have questioned the CRA’s level of service and processes surrounding SR&ED objections. Today, the CRA p...